Investments play crucial role in financial planning for a secure life ahead. Many people take comfort in investing surplus cash in fixed deposits. Valuing convenience and security associated with Fixed deposits (FDs), they altogether ignore investments in company stocks and equity mutual funds. The question is whether it is the right approach? Should equity investments be entirely overlooked? Read on…

Many risk averse investors rely on FDs on account of their safety, convenience and assured returns. However, avoiding risks and relying fully on FDs may not augur well with the objective of overall financial well-being. Understanding the differences between the investments in FDs and equity will help us to make informed decisions aligned with our financial goals. Let us compare and contrast both the options:

• Time Horizon

While FDs have fixed tenures running from a few weeks to several years, equity investments may have perpetual existence

Equity shares represent ownership in a company. FDs typically have a fixed maturity date. Equity shares do not have an expiration date. They continue with the company that has perpetual existence.

• Knowledge required

Investing in FDs require basic knowledge. On the other hand, investing in equity shares require deeper knowledge.

FDs are easy to understand simple instruments with predictable returns. Investors need to have basic understanding of interest, tenures and taxes. On the other hand, equity investments require deeper knowledge of dividends, capital gains, businesses, industries, and environment. However, investors may choose equity mutual funds to overcome lack of knowledge.

• Risk

The risks associated with FDs are lower than that with equities.

FDs are favourite of many on account of low risks. However, it is important to be aware that in case of Bank failures investors may lose their money. They may only be able to get a sum up to ₹5 lakh per depositor, per bank from Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India. Further, careful selection of stocks from reputed large cap / blue chip companies can help lower risks of equity investments.

• Returns

The FDs provide fixed interest rates. The returns in case of equities are volatile and range from losses to astronomically high returns.

It has been observed that careful equity investments offer higher returns over time. Overall equity markets may easily provide returns in the range of 10% to 15%. On the other hand, FDs provide interest at much lower rates which are typically between 6%-8% per annum.

• Taxation

Interest from FDs is taxed every year as per income tax slab on the basis of interest accrued. Equity returns in form of short-term or long-term capital gains are taxed in the year of sale

The rates of taxes for short-term and long-term capital gains are 20% and 12.5% respectively, excluding surcharges and cess. Using equity alternatives wealth can be built without paying annual taxes as there is no tax implication on capital appreciation. Capital gains accrue in the year of sale only if sold. However, dividends are taxed as per normal rates as per income tax bracket. Equity investments offer tax efficiency for long-term investors unlike FDs where tax burden is high for people in high tax bracket.

• Liquidity

Unlike popular belief, FDs have lower liquidity considering penalties on premature withdrawal with lower interest rates.

FDs are not ideal for immediate access to money. Equity investments can be redeemed to avail cash without penalties. However, sudden price drops may affect the amount realized.

Impact of inflation and taxes on FDs and equity investments

A major challenge in solely relying on FDs is that they are not inflation friendly. Adjusted for taxes and inflation, the returns from fixed deposits can easily be negative. Inflation reduces the purchasing power of money, diminishing the real returns from FDs. Returns may turn negative when inflation is more than the interest earned. Carefully selected equity investments have the potential to outpace inflation, providing better capital growth.

An interest rate of seemingly high 7% in case of FDs can actually turn out to be a loss. Consider below:

| Investment | ₹ 1,00,000 |

| Interest @ 7% | ₹ 7,000 |

| Tax @ 24% | ₹ 1,680 |

| Actual return after tax | ₹ 6,320 |

While actual returns will depend upon the period of investment, interest rate and applicable tax rate, in the above example, the returns amount to 6.3% and not 7%. After adjusting for inflation, there can be situation of negative returns.

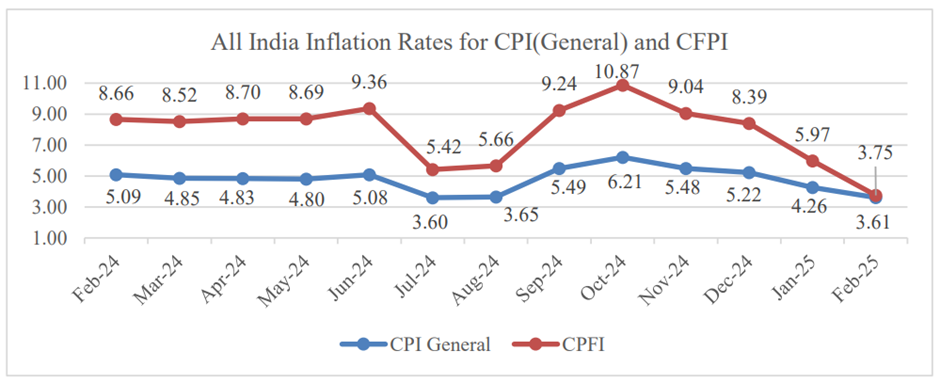

In the chart below, you can see high inflation rates (Blue Line). consider the inflation rate of 6.2 % in the month of October, 2024 which is almost at par with the returns from the FDs. Thus there was almost no return. The actual returns are only marginal in other months as well. Further the food inflation (Red line) is way above the interest rates in most of the months, seriously impacting the purchasing power, at least in case of food items.

Source: National Statistics Office, Ministry of Statistics and Programme Implementation. All India inflation rates for CPI (Consumer Price Index) and CFPI (Consumer Food Price Index). Figures for February, 2025 is provisional.

Conclusion

It is important for investors to have a mix of both equities and FDs, to have stability, growth, and protection against inflation. By having the right balance, they can find ways through life uncertainties and achieve long-term financial security within the dynamic environment. Skepticism against equity is a bias that must be overcome for overall financial wellbeing.

Combining FDs and equity creates a resilient corpus that adapts to uncertainties. While FDs anchor with safety and liquidity, equity propels toward higher wealth.

Also read: